All it takes is a few clicks.

200+

Years Proudly Serving Our Customers

1MM+

Small Business Customers

14x

ETHISPHERE: World's Most Ethical Company**

What Is Professional Liability Insurance?

Professional liability insurance protects businesses when employees make mistakes in the professional services they’ve provided to customers or clients. This coverage is also known as errors and omissions insurance (E&O). Even if you’re an expert in your business, mistakes happen. And if your client or customer thinks a mistake in your professional services caused a financial loss, they can sue you.

What Does Professional Liability Insurance Cover?

Professional liability insurance for small businesses can help protect against claims of:

- Negligence: If services you or your company provided result in damage or injury to a client.

- Misrepresentation: If a client claims that false or misleading information convinced them into a contract agreement with you or your company, which lead to damages to the client.

- Inaccurate advice: If a customer claims you provided advice that caused them damage.

- Personal injury: If someone accuses you or your business of libel or slander, whether it’s true or not.

- Copyright Infringement: If someone claims you or your business used their copyrighted work without their permission.

- Defense costs: Professional liability insurance can help cover your defense costs if a client sues you for mistakes in the professional services you provided them. Defense costs include attorney fees and other court-related expenses.

Even if you didn’t do anything wrong and believe you’ve made no mistakes, your client can still sue your business. Without coverage, you’ll have to pay expensive legal defense costs out of pocket.

What Professional Liability Insurance Doesn’t Cover

Professional liability insurance doesn’t cover every kind of claim. It won’t help your business with claims of:

- Bodily injury or property damage: You’ll want to get a general liability insurance policy to help cover claims that your business hurt somebody or damaged their property.

- Work-related injuries or illnesses: If your employees get hurt or sick from their job, you’ll need a workers’ compensation insurance policy to help them recover and return to work.

- Data breach: If your business loses personally identifiable information (PII), data breach insurance can help you respond to the breach. Some insurers call this coverage cyber liability insurance.

How Professional Liability Insurance Works

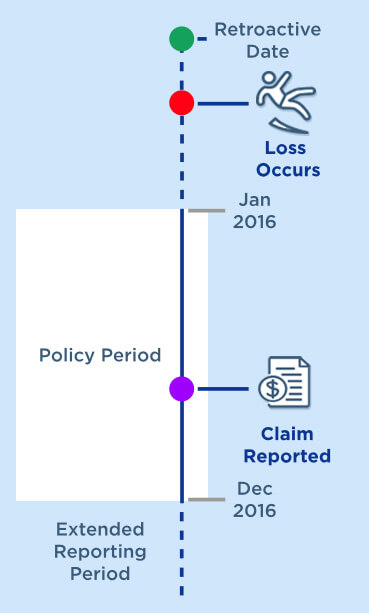

Many insurance companies write a professional liability insurance policy on a claims-made basis with a retroactive date and extended reporting period.

The retroactive date means you’re covered for incidents that happen on or after a specified date in your policy.

The extended reporting period helps cover claims filed within a certain time after your policy expires. This is generally a 30- to 60-day period, but you can extend this period to a year or more for an additional cost.

Your insurance company only covers claims against your business during your policy period within the extended reporting period. And the claim must be from a covered error or omission that happened after your policy’s retroactive date. It can help cover:

- Damages

- Legal defense costs

- Disciplinary proceedings

- Loss of earnings

- Subpoena assistance

Some policies can also be written on an occurrence policy. This means there will be coverage for losses that happen during your policy period, even if the claim gets reported after your policy expires.

CLAIMS-MADE EXAMPLE

Since the claim was reported during the policy period and the loss occurred after the retroactive date, it would be eligible for coverage under a claims-made policy.

If a claim is brought after the policy’s expiration, it can get coverage if it’s reported within the extended reporting period.

Who Should Get a Professional Liability Policy?

You may be wondering who needs professional liability insurance. It’s an important coverage that business owners who provide a service to a client or customer should have. You’ll want to get professional liability insurance coverage if you:

- Have to sign a contract that requires you to carry coverage

- Offer professional services directly to customers

- Regularly give advice to clients

Be aware that some states require this type of business insurance.

Even insurance agents need liability protection, which is why The Hartford offers E&O insurance for insurance agents.

A Big Help for Small Business Owners

Interior Design Business

Jane owns an interior design business. Recently, a client's custom furniture didn't fit and now Jane is being sued. Luckily, Jane is an insured professional and has a Business Owner's Policy with professional liability insurance, which will help pay for her legal fees.

Many small business owners don’t realize the big benefits of professional liability insurance.

States and hospitals require healthcare professionals to carry professional liability insurance.

How Does It Help?

Professional liability insurance protects against common claims like negligence, misrepresentation and inaccurate advice. It will also help cover violations of good faith and fair dealing. If a client sues you, this policy may help pay your legal expenses.

To learn more about professional liability insurance, get a quote from us today.

Looking for Professional Liability Insurance Coverage?

The Hartford makes it easy to get a professional liability insurance quote online.

How Much Does Professional Liability Insurance Cost?

Your cost is unique to your business. What you pay for professional liability insurance will vary by product, limits chosen and risk class or hazard group of your business.

| Product | Avg. Minimum Monthly Premium*** | |

|---|---|---|

| Misc. Professional Liability Standalone Coverage | $300 | |

| Misc. Professional Liability Endorsements | $150 | |

| Architects and Engineers Professional Liability | $1,700 | |

| Healthcare Professionals Professional Liability | Varies depending on type of practice, $300-$1,500 | |

| Errors & Omissions Insurance for Technology Companies | Varies by state, $350-500 |

*** Quotes will vary by business depending on the size of your business, the state your business is located in, coverage limits chosen, and the risk class your business is associated with.

Factors that can impact your professional liability insurance cost include:

- Policy details, like coverage limits

- Type of business

- Location

- Business size, number of employees and clients

- Years in business

- Claims history

When you’re ready to get a professional liability insurance quote, it’s a good idea to have important business documents on hand, such as:

- Copies of contracts

- Documentation procedures

- Any information about previous errors and omissions coverage

- Quality control processes

- Employee training initiatives

You can work with our specialists to get the right amount of errors and omissions (E&O) insurance coverage for your business. Backed by more than 200 years of experience, we can help protect you with professional liability insurance for small business.

Your Fast and Free Quote Is Here

Get the professional liability insurance you need to protect your business.

Find Out More About Professional Liability Insurance

Additional Content

Liability coverage is required if you want to protect yourself from potential legal action.

Other Business Coverages

We offer insurance coverages for companies of all sizes – large and small.

Last Updated: May 5, 2023

** "World's Most Ethical Companies" and "Ethisphere" names are registered trademarks of Ethisphere LLC.

Additional disclosures below.